Click here to access this dispatch as a formatted PDF.

This report was written by Andrei Stetsenko based on underlying research conducted jointly with our Mumbai-based analyst Nireeksha Makam.

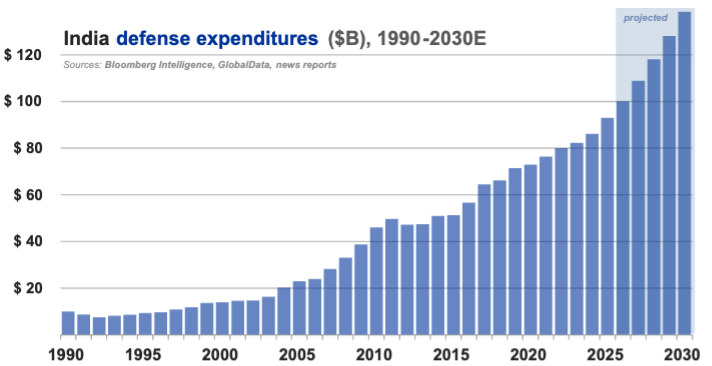

India is the world’s 5th-largest military spender, behind the U.S., China, and Russia, and roughly on par with 4th-place Germany.

- India’s defense outlays account for roughly 3% of the global total (up from 2% two decades ago), and are equivalent to just over 2% of Indian GDP.

- India outspends Pakistan on defense nearly nine-fold, despite the latter’s allocation to defense of a higher share of its drastically smaller GDP.

- However, India must play catch-up to China, whose defense outlays account for 12% of the global total – but just ~1.7% of China’s much greater GDP.

- In 2020, a brief but intense border conflict along India’s Himalayan frontier with China – commonly referred to in India as the Ladakh standoff – resulted in multiple fatalities on both sides.

Equipment acquisitions account for less than 30% of Indian defense expenditure.

- The lion’s share of India’s defense budget continues to be allocated toward salaries, pensions, maintenance, and related operational line items.

- More than half of Indian military outlays go toward salaries, day-to-day operational costs, and pensions for the nation’s ~1.4mm active-duty troops and ~3.4mm defense pensioners.

- More than half of Indian military outlays go toward salaries, day-to-day operational costs, and pensions for the nation’s ~1.4mm active-duty troops and ~3.4mm defense pensioners.

- In the aftermath of the May 2025 four-day armed conflict with Pakistan known in India as Operation Sindoor, the Indian government moved to provide the armed forces with ₹500B (≈ $6B) in emergency/supplemental funding for replenishing munitions and boosting defense R&D.

- That military operation was a direct response to the Pahalgam terrorist attack in India’s Jammu and Kashmir region.

India is the world’s second-largest arms importer, only slightly trailing Ukraine.

- Russia’s share of Indian arms imports has drastically declined in recent years – from nearly three-quarters a decade ago to just over one-third today.

- This shift has been driven by a combination of Indian decisionmakers’ increasing preference for high-tech American, French, and Israeli weapons (see below), Russian weaponry’s poor performance on the battlefields of Ukraine, and concerns with respect to the timely availability and reliability of Russian supplies (particularly of critical spare parts).

- The shift away from Russia has been most rapid in the case of India’s air force and navy; by contrast, India’s army continues to rely on large numbers of Russian-made armored vehicles.

- This shift has been driven by a combination of Indian decisionmakers’ increasing preference for high-tech American, French, and Israeli weapons (see below), Russian weaponry’s poor performance on the battlefields of Ukraine, and concerns with respect to the timely availability and reliability of Russian supplies (particularly of critical spare parts).

In 2016, the United States designated India a “major defense partner,” clearing the way for India’s defense industry to access advanced U.S. military technology.

- Over the past decade, India cumulatively imported ~$30B worth of military hardware from the U.S., including helicopters, transport planes, and drones.

- In 2023, Hindustan Aeronautics (NSE: HAL) struck a deal with GE Aerospace (NYSE: GE) to jointly manufacture jet engines in India.

- While the Trump administration’s aggressively punitive tariff strategy WRT India has been overshadowing the until-recently deepening U.S.-India relationship, the two nations are staying the course when it comes to practical examples of major defense cooperation – most notably, in the form of recently-concluded naval drills by the so-called “Quad” of Australia, Japan, India, and the United States.

- Diplomatic maneuvering reportedly happening behind the scenes may clear the way for India to buy F-35s (currently exported only to America’s closest allies) – in part to deter any Indian purchase of Russia’s alternative Su-57.

- In the meantime, India is drawing closer with other long-standing foreign partners – most notably, France and Israel.

- The unrivaled combination of macro tailwinds underpinning the world’s fastest-growing major economy (including plentiful low-cost labor and abundant skilled engineering talent) makes India attractive to Western defense/aerospace companies both as a supplier (see below) and as an increasingly bountiful end-market for their products.

- France and Israel collectively supply nearly half of India’s arms imports, and India is by far the largest export customer for France’s defense contractors.

- In August 2025, the Indian government announced the launch of a collaboration with France’s Safran (EPA: SAF) to develop jet engines for India’s planned indigenous fifth-generation fighter aircraft.

India’s has become less reliant on imported arms in recent years, while steadily bolstering its ability to indigenously design and produce a range of platforms including armored vehicles, helicopters, warships, and submarines.

- India’s remaining dependencies relate primarily to cutting-edge technologies such as the latest generation of stealth aircraft.

As part of its Atmanirbhar Bharat (“Self-Reliant India”) policy, the Modi government has rolled out policies designed to incentivize the development of locally-built substitutes for imported systems, sub-systems, and components.

- Foremost among these are minimum thresholds (typically at least 50%) for the share of content that must be sourced indigenously for any contracts awarded as part of the nation’s defense procurement.

- Foreign defense/aerospace firms seeking to qualify under these rules typically seek out one or more Indian offset partners (IOPs) capable of manufacturing key components within India.

- Foreign defense/aerospace firms seeking to qualify under these rules typically seek out one or more Indian offset partners (IOPs) capable of manufacturing key components within India.

- For example, the HAL Tejas combat aircraft platform assembled by Hindustan Aeronautics (NSE: HAL) contains >60% indigenous content, with the remainder attributable to imported components including F404 jet engines supplied by GE Aerospace (NYSE: GE).

- The Tejas program dates back to the 1980s, when India persuaded Ronald Reagan to supply India with advanced jet engines and “fly-by-wire” electronic control technology.

- The Tejas program dates back to the 1980s, when India persuaded Ronald Reagan to supply India with advanced jet engines and “fly-by-wire” electronic control technology.

- As part of the same Defence Acquisition Procedure 2020 reforms that hiked indigenous content thresholds, the Modi government raised the limit on foreign ownership of defense firms from 49% to 74%.

- This move was intended to facilitate joint ventures and technology transfers between Indian companies and foreign partners.

The Indian government has made it a priority to accelerate defense contracting processes, including by facilitating more direct businesses between the Indian military and smaller, more nimble private-sector contractors such as those discussed further down in this memo.

- Top priorities include electronic warfare systems, long-range missiles, fighter jets, autonomous/ uncrewed technologies, and air defense/anti-drone systems.

- India’s Ministry of Defense has initiated a major modernization effort “aimed at breaking longstanding institutional silos, fast-tracking emergency procurements and shifting towards new domains like cyber, space, artificial intelligence (AI), hypersonics, and robotics.”

{kind=link}

The Indian government’s stated policy is to nurture a domestic defense-industrial base that is successful enough – meaning, profitable enough – to not only fulfill contracts, but also be counted on to service Indian-made products for years and years down the line, while simultaneously investing in the kind of capacity expansions and high-level R&D required to eventually make India fully self-reliant with respect to even the most technologically advanced defense systems.

- As part of this policy, the government has mandated that at least 25% of defense procurement and R&D funds be earmarked for private-sector players.

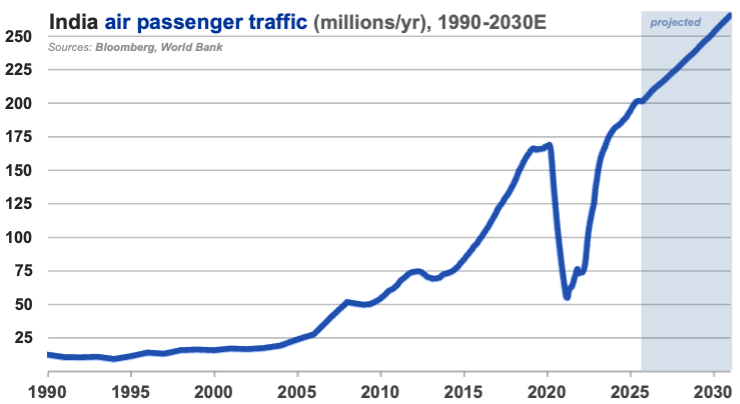

India recently became the world’s 3rd-largest aviation market in terms of passenger traffic (behind only the U.S. and China) – up from 8th just a decade ago.

- Even after recent years’ rapid growth, Indians today take just ~0.14 yearly flights per capita – equivalent to less than a quarter of the ~0.6 global average.

- India’s nascent maintenance, repair, and overhaul (MRO) industry currently captures only a small fraction of its addressable market, with the vast majority of Indian-owned aircraft/aero-engines relying on overseas servicing.

- In 2025, the Indian government announced plans to more than double the country’s number of airports, from 162 as of this writing to 350 by the year 2047.

Historically, India’s defense/aerospace industry has been dominated by a trio of relatively inefficient incumbents that, while publicly listed, remain majority-owned by and firmly under the control of the Indian government.

- Hyderabad-based Bharat Dynamics (NSE: BDL) is India's sole indigenous manufacturer of missile and torpedo systems.

- Bengaluru-based Bharat Electronics (NSE: BEL) manufactures avionics, night-vision equipment, radar systems, and other electronics, primarily for defense/aerospace applications.

- Bengaluru-based Hindustan Aeronautics (NSE: HAL) designs and manufactures aircraft, helicopters, and related systems, including indigenous HAL Tejas combat aircraft, Su-30 jets made under license from Russia’s Sukhoi, and a new-generation fighter aircraft (known as HAL AMCA) expected to be produced in partnership with U.S. and/or European defense contractors.

Another trio of listed but state-controlled businesses specialize in shipbuilding:

- Mumbai-based Mazagon Dock Shipbuilders (NSE: MAZDOCK) manufactures warships and submarines.

- Kochi-based Cochin Shipyard (NSE: COCHINSHIP) specializes in aircraft carriers and other large, complex vessels.

- Kolkata-based Garden Reach Shipbuilders (NSE: GRSE) builds warships, as well as commercial vessels for both domestic and export customers.

Within the more dynamic private sector, leading defense/aerospace firms include:

- Ahmedabad-based Adani Defence & Aerospace – a subsidiary of Adani Enterprises (NSE: ADANIENT).

- The defense division of Pune-based Bharat Forge (NSE: BHARATFORG).

- Mumbai-based Godrej Aerospace – a subsidiary of the unlisted holdco known as Godrej & Boyce Mfg.

- The defense division of Mumbai-based Larsen & Toubro (NSE: LT).

- In 2017, LT established L&T MBDA Missile Systems, a joint venture with European missile manufacturer MBDA with the objective of developing and supplying state-of-the-art missile systems to the Indian military.

- In 2017, LT established L&T MBDA Missile Systems, a joint venture with European missile manufacturer MBDA with the objective of developing and supplying state-of-the-art missile systems to the Indian military.

- Mahindra Aerospace – part of Mahindra & Mahindra (NSE: M&M).

- In 2024, Bengaluru-based Mahindra Aerospace’s wholly-owned subsidiary Mahindra Aerostructures entered into a multi-year agreement with Airbus (EPA: AIR) to produce components for the entire Airbus range of civil aircraft.

- In 2025, Mahindra Aerospace’s wholly-owned subsidiary Mahindra Aerostructures won a contract to manufacture the main fuselage of Airbus's best-selling H125 helicopter.

- The aerospace division of Noida-based Samvardhana Motherson International (f.k.a. Motherson Sumi Systems – NSE: MOTHERSON).

- MOTHERSON entered the aerospace market via its 2022 acquisition of a majority stake in Bengaluru-based CIM Tools (a growing supplier to Airbus) and its 2024 acquisition of France-based aero-engine components manufacturer AD Industries (subsequently renamed Motherson Aerospace).

- MOTHERSON entered the aerospace market via its 2022 acquisition of a majority stake in Bengaluru-based CIM Tools (a growing supplier to Airbus) and its 2024 acquisition of France-based aero-engine components manufacturer AD Industries (subsequently renamed Motherson Aerospace).

- Mumbai-based Reliance Defence – a subsidiary of Reliance Infrastructure (NSE: RELINFRA).

- In 2017, Reliance Defence established Dassault Reliance Aerospace (DRAL), a joint venture with France’s Dassault Aviation (EPA: AM).

- In 2018, Reliance Defense set up Thales Reliance Defence Systems (TRDS), a joint venture with France’s Thales (EPA: HO) tasked with developing radar and electronic warfare systems.

- In 2017, Reliance Defence established Dassault Reliance Aerospace (DRAL), a joint venture with France’s Dassault Aviation (EPA: AM).

- New Delhi-based Tata Advanced Systems (a.k.a. TASL) – a subsidiary of the unlisted holdco known as Tata Sons.

- In 2010, TASL set up Tata Lockheed Martin Aerostructures (TLMAL), a joint venture with Lockheed Martin (NYSE: LMT) that started out as a supplier of components for C-130J Super Hercules military transport aircraft.

- In 2015, TASL set up Tata Boeing Aerospace (TBAL), a joint venture with Boeing (NYSE: BA) that now supplies fuselages for Apache helicopters.

- In 2024, TASL and Airbus (EPA: AIR) inaugurated a final assembly line for the C295 military aircraft in Vadodara, Gujarat.

- In 2025, TASL announced a partnership with Dassault Aviation (EPA: AM) to manufacture key components of the Rafale fighter jet in India.

- In 2010, TASL set up Tata Lockheed Martin Aerostructures (TLMAL), a joint venture with Lockheed Martin (NYSE: LMT) that started out as a supplier of components for C-130J Super Hercules military transport aircraft.

- The aerospace division of Bengaluru-based Wipro Enterprises, the unlisted parent company of various non-IT businesses controlled by Azim Premji, the founder of IT giant Wipro (NSE: WIPRO).

Listed private-sector Indian firms specializing in aerostructures, precision-engineered aerospace components, and/or aerospace machine tools include:

- Belgaum-based Aequs (NSE: AEQUS);

- Hyderabad-based Azad Engineering (NSE: AZAD – see below);

- Bengaluru-based Dynamatic Tech. (NSE: DYNAMATECH – see below);

- Lucknow-based PTC Industries (NSE: PTCIL);

- Hyderabad-based MTAR Tech. (NSE: MTARTECH);

- Bengaluru-based Sika Interplant Systems (BSE: 523606 – see below); and

- Bengaluru-based Unimech Engineering (NSE: UNIMECH – see below).

Listed private-sector Indian firms specializing in defense-related electrical, electronic/avionic, and/or electromechanical products include:

- Hyderabad-based Apollo Micro Systems (NSE: APOLLO);

- Hyderabad-based Astra Microwave (NSE: ASTRAMICRO – see below);

- Hyderabad-based Avantel (NSE: AVANTEL);

- Bengaluru-based Axiscades Tech. (NSE: AXISCADES);

- Bengaluru-based Centum Electronics (NSE: CENTUM);

- Chennai-based Data Patterns (NSE: DATAPATTNS);

- Bengaluru-based DCX Systems (NSE: DCXINDIA – see below);

- Navi Mumbai-based Paras Defence & Space Tech. (NSE: PARAS); and

- Bengaluru-based Rossell Techsys (NSE: ROSSTECH).

Despite its status as one of the world’s largest and fastest-growing markets for aircraft, maintenance services, and parts, India still accounts for less than 2% of global aerospace supply chains.

- Analysts expect India’s share of global aerospace supply chains to expand rapidly – potentially more than quintupling within a decade to 10%.

“Our engine volumes are growing at around 20% and the traditional supply chains are just not able to support it […while] India is the best solution to supply chain challenges […and] the best cost market.”

– Huw Morgan, Rolls-Royce SVP for aerospace procurement

Gymkhana’s defense/aerospace portfolio companies are benefiting from India’s increasing attractiveness to multinational firms as both a burgeoning source of demand and as a manufacturing hub.

- Several of our defense/aerospace portfolio companies are suppliers of critical components to leading multinationals such as Airbus (EPA: AIR), Boeing (NYSE: BA), and/or Rolls-Royce (LSE: RR), whose accelerating shift toward Indian suppliers is being driven in part by frustration with labor and supply chain disruptions constraining output at their existing, relatively high-cost plants.

- Airbus currently sources >$1B in components annually from India, with plans to double that within five years to $2B.

- 100% of Airbus commercial aircraft produced today incorporate made-in-India components and technologies.

- Boeing currently sources >$1B in components annually from India, up >4x from a decade ago.

- Rolls-Royce reportedly plans to double sourcing from India within five years.

- Airbus currently sources >$1B in components annually from India, with plans to double that within five years to $2B.

- In many cases, our defense/aerospace portfolio companies are not only increasing revenues, but also steadily shifting their businesses up the value chain into larger, more complex, and typically more lucrative sets of products.

- Businesses such as Dynamatic Tech. (NSE: DYNAMATECH – see below) and Astra Microwave (NSE: ASTRAMICRO – see below) are evolving from mere component suppliers into partners trusted by the U.S./European airframe and aero-engine giants to develop, integrate, and reliably deliver expanding shares of increasingly sophisticated systems.

- This progression up the value chain generally implies even stickier customer relationships, more formidable qualification/entry barriers deterring any would-be competitors, and of course more lucrative economics.

Gymkhana Partners has roughly one-tenth of its capital invested in Indian defense/aerospace businesses.

- The following pages briefly introduce six of these companies; in our view, all six have laid the foundations for growth into world-class defense/aerospace businesses worth many times their current market capitalizations.

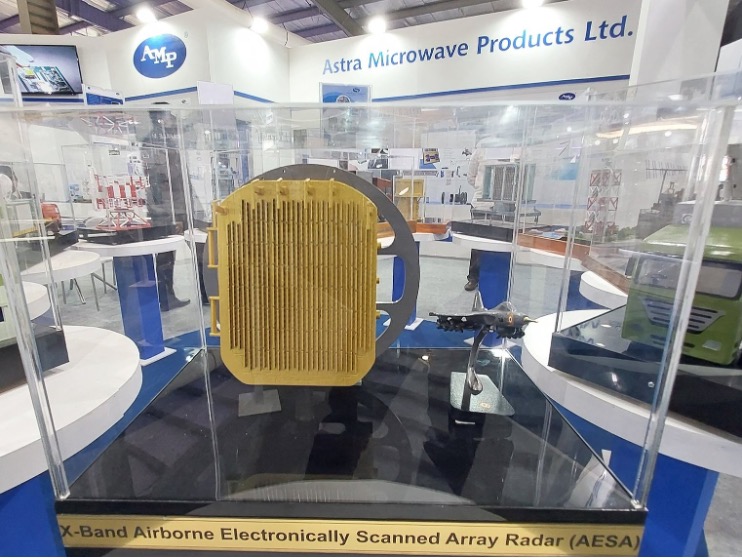

Astra Microwave Products (NSE: ASTRAMICRO; Bloomberg: ASTM IN; also known by the acronym AMPL) develops and supplies increasingly sophisticated antennas, receivers, radars, and electronic warfare systems.

- As of December 17, 2025, Hyderabad-based ASTRAMICRO has a market capitalization of ~₹85 billion (≈ $935 million).

- ASTRAMICRO generates annual revenue of ~₹12 billion (≈ $130 million); sales have approximately doubled over the past five years.

- Andrei and Nireeksha have visited ASTRAMICRO twice: first in February 2025 and more recently in November 2025.

- In 2015, ASTRAMICRO established Astra Rafael Comsys, a joint venture with Israel’s state-controlled Rafael Advanced Defense Systems focused on advanced radios and electronic warfare systems.

- In October 2025, India’s Defense Research and Development Organisation (DRDO) formally inducted ASTRAMICRO into a consortium tasked with integrating indigenously-developed Virupaksha active electronically scanned array (AESA) radar systems into the air force’s Su-30MKI fleet (as replacements for those jets’ existing Russian-made radars).

- Our research suggests that the only other listed Indian company with substantially overlapping defense electronics capabilities is Bengaluru-based Centum Electronics (NSE: CENTUM).

Azad Engineering (NSE: AZAD; Bloomberg: AZAD IN; also known by the acronym AEL) supplies precision-forged and machined components to customers including GE, Honeywell, Rolls-Royce, Safran, and Siemens.

- As of December 17, 2025, Hyderabad-based AZAD has a market capitalization of ~₹102 billion (≈ $1.1 billion).

- AZAD generates annual revenue of ~₹6 billion (≈ $66 million); sales have approximately doubled over the past three years, and are on track to more than double again over the next three years.

- Andrei and Nireeksha visited AZAD in November 2025.

- AZAD’s order backlog of >₹65 billion (≈ $720 million) is equivalent to more than 10x the company’s current annual sales.

- The capacity expansions required to fulfill this overflowing orderbook include multiple recently-inaugurated facilities at AZAD’s expanding manufacturing plant located in Tuniki Bollaram, Telangana.

“Earning the trust of an OEM — especially for life-critical and highly engineered components — requires years of consistent performance, precision, and reliability, not just by simply acquiring technology […] Having demonstrated these capabilities over time consistently, we now enjoy the confidence of our global aerospace and defence customers, who entrust us with long-term contracts.”

– Rakesh Chopdar, Azad Engineering chairman and CEO

- In October 2024, North Carolina-based Honeywell (NASDAQ: HON) awarded AZAD a contract to supply complex aerospace components.

- In November 2024, AZAD won a contract from Japan-based Mitsubishi Heavy Industries (TYO: 7011); this multiyear contract (including both the initial phase and a second phase announced September 2025) has an estimated value of ~$156 million – more than double AZAD’s current annual revenue.

- In February 2025, U.K.-based Rolls-Royce (LSE: RR) signed a seven-year deal to source critical defense aero-engine components from AZAD.

- In February 2025, Rolls-Royce awarded AZAD a separate multi-year contract for critical commercial aero-engine components.

- In February 2025, Rolls-Royce awarded AZAD a separate multi-year contract for critical commercial aero-engine components.

- In May 2025, Massachusetts-based GE Vernova (NYSE: GEV) signed a six-year deal to source advanced nuclear/thermal power airfoils from AZAD.

- In November 2025, AZAD entered into a long-term agreement to supply aero-engine components to Pratt & Whitney (a subsidiary of Virginia-based RTX Corp. – NYSE: RTX).

{kind=link}

DCX Systems (NSE: DCXINDIA; Bloomberg: DCXINDIA IN) is an aerospace electrical systems specialist with an expanding partnership with Lockheed Martin.

- As of December 17, 2025, Bengaluru-based DCXINDIA has a market capitalization of ~₹17 billion (≈ $190 million).

- DCXINDIA generates annual revenue of ~₹13 billion (≈ $150 million); sales have approximately doubled over the past five years.

- DCXINDIA management are confident of growing revenue at a +20%-25% compound annual rate while substantially expanding margins.

- Andrei has visited DCXINDIA twice: first (along with Steve) in December 2023 and more recently (along with Nireeksha) in November 2024.

- DCXINDIA generates annual revenue of ~₹13 billion (≈ $150 million); sales have approximately doubled over the past five years.

- Established in 2011 as a supplier of aerospace cables and wire harnesses, DCXINDIA has progressed up the value chain into more advanced parts.

- DCXINDIA has long-established partnerships with Israel’s state-controlled aerospace manufacturer IAI, as well as with ELTA Systems, an IAI subsidiary specializing in advanced electronics.

- DCXINDIA also boasts a deepening relationship with Maryland-based Lockheed Martin (NYSE: LMT).

- In February 2024, DCXINDIA received an initial ~$2mm pilot order from LMT; later that year, DCXINDIA announced the first in what is expected to be a series of much larger commercial orders from LMT worth tens of millions of dollars each.

- In February 2024, DCXINDIA received an initial ~$2mm pilot order from LMT; later that year, DCXINDIA announced the first in what is expected to be a series of much larger commercial orders from LMT worth tens of millions of dollars each.

- A relevant analogue/comp to DCXINDIA is Bengaluru-based Rossell Techsys (NSE: ROSSTECH).

Dynamatic Technologies (NSE: DYNAMATECH; Bloomberg: DYTC IN; also known by the acronym DTL) is a supplier of increasingly complex/mission-critical components to customers including Airbus, Boeing, and Dassault Aviation.

- As of December 17, 2025, Bengaluru-based DYNAMATECH has a market capitalization of ~₹61 billion (≈ $675 million).

- DYNAMATECH generates annual revenue of ~₹15.5 billion (≈ $170 million); sales are on track to grow at a double-digit rate for the foreseeable future.

- Andrei, Steve, and Nireeksha visited DYNAMATECH in November 2025.

- Incorporated in 1973 as a manufacturer of hydraulic pumps, DYNAMATECH subsequently expanded into aerospace components.

- DYNAMATECH began supplying parts to Hindustan Aeronautics (NSE: HAL) in the early 2000s.

- In 2010, DYNAMATECH became a supplier to Boeing (NYSE: BA), and soon after won contracts to supply critical parts for the CH-47 Chinook helicopter.

- Over roughly the same period, DYNAMATECH began supplying flap track beams to Airbus (EPA: AIR) for its A320 and A330 jets.

- In 2015, Airbus gave DYNAMATECH the largest manufacturing contract it had ever awarded to any Indian private-sector company.

- In 2024, Airbus awarded DYNAMATECH a contract to manufacture all door variants for all A220 planes worldwide, in one of the largest-ever aerospace export contracts won by an Indian company.

- In recent years, DYNAMATECH has won long-term contracts to supply critical parts for aircraft including Boeing’s F-15EX Eagle II fighter and France-based Dassault Aviation’s (EPA: AM) Falcon line of business jets.

- DYNAMATECH’s wholly-owned subsidiary Dynauton Systems specializes in unmanned aerial vehicles (UAVs); examples include its indigenously-developed Kaatil loitering munition (a.k.a. “kamikaze drone”).

Sika Interplant Systems (BSE: 523606; Bloomberg: SIKA IN; a.k.a. “SIKA”) manufactures and services an array of critical aerospace components.

- As of December 17, 2025, Bengaluru-based SIKA has a market capitalization of ~₹19 billion (≈ $210 million).

- SIKA generates annual revenue of ~₹2.1 billion (≈ $23 million); sales have approximately doubled over the past four years.

- SIKA generates annual revenue of ~₹2.1 billion (≈ $23 million); sales have approximately doubled over the past four years.

- Founded in 1969, SIKA is set to benefit from rapid growth in India’s aerospace components and maintenance, repair, and overhaul (MRO) markets.

- SIKA’s MRO business, a leading driver of the overall company’s revenue growth, is expanding its share of India’s booming MRO market.

- The company’s other businesses supply and maintain landing gear, interconnection systems, avionics, ground support equipment, and tools related to disaster management/search and rescue.

- In 2014, Kunal Sikka (son of the chairman Rajeev Sikka) left his prior career at Goldman Sachs in order to join SIKA as CFO; he became CEO in 2021.

- According to one analyst, “the metamorphosis of SIKA started” when Kunal joined the business and “brought in the required financial discipline”.

- According to one analyst, “the metamorphosis of SIKA started” when Kunal joined the business and “brought in the required financial discipline”.

- SIKA has extensive underutilized land holdings in/around Bengaluru; our research suggests that two parcels with a combined reported value on SIKA’s balance sheet of ~₹255mm (≈ $3mm) would, if monetized, command a market value equivalent to a significant fraction of the company’s entire market capitalization.

- In 2017, SIKA and U.K.-based MRO provider Aerotek Aviation Engineering established a joint venture to offer landing gear MRO services from a dedicated facility within Sika’s Bengaluru campus.

- In April 2025, SIKA was appointed as an authorized provider of MRO services on behalf of Radiant Power (a subsidiary of Florida-based HEICO – NYSE: HEI).

- In June 2025, SIKA entered into a license agreement with Collins Aerospace (a subsidiary of Virginia-based RTX Corp. – NYSE: RTX) that will allow SIKA to undertake MRO of certain Collins-manufactured flight control components installed on all Airbus (EPA: AIR) A320/A321 aircraft.

Unimech Aerospace (NSE: UNIMECH; Bloomberg: UNIMECH IN; also known by the acronym UAML) produces mission-critical aero-engine and airframe machine tools.

- As of December 17, 2025, Bengaluru-based UNIMECH has a market capitalization of ~₹47 billion (≈ $515 million).

- UNIMECH generates annual revenue of ~₹2.7 billion (≈ $30 million); sales have approximately tripled over the past three years.

- Andrei and Nireeksha visited UNIMECH in Nov. 2025.

- Established in 2016 by a team of five co-founders, UNIMECH (a portmanteau of “universal” and “mechanical”) supplies machine tools to customers including Airbus (EPA: AIR), Boeing (NYSE: BA), Pratt & Whitney (a subsidiary of RTX Corp. – NYSE: RTX), Rolls-Royce (LSE: RR), and the GE Aerospace-Safran joint venture known as CFM International.

- Analysts estimate UNIMECH is able to profitably undercut its North American and European competitors by ~15%-20%.

- Analysts estimate UNIMECH is able to profitably undercut its North American and European competitors by ~15%-20%.

- UNIMECH is in the process of substantially expanding its Bengaluru manufacturing footprint, in part to accommodate a nascent but very promising business line supplying complex parts to the Nuclear Power Corp. of India.

Legal information and disclosures

The views expressed are the views of the author as of the date indicated on each posting; such views are subject to change without notice. Farley Capital L.P. (Farley Capital)has no duty or obligation to update the information contained herein. Further, Farley Capital makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Any discussion regarding investment returns or financial projections are provided as illustrative examples only and no inference shall be made therefrom regarding the potential for returns on any investment discussed. Moreover, you should be aware that all types of investments involve a significant degree of risk, and wherever there is potential for profit, there is also the possibility of loss.

This content is being made available for informational and educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as financial, legal, or tax advice, or as an offering of advisory services. The information contained herein shall not constitute an offer to sell, or a solicitation to subscribe for, interests in any investment vehicle managed by Farley Capital, which offer or solicitation will only be made to qualified investors and accompanied by a private placement memorandum, subscription agreement, and other related offering documents. Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Farley Capital believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy or completeness of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

This content, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of Farley Capital.

Past performance of Gymkhana Partners and any funds managed by Farley Capital L.P. (collectively, the “Funds”) is not indicative of future results. No representations or warranties of any kind are made or intended, and none should be inferred, with respect to the economic return or the tax consequences from a potential investment in the Funds. Each investor should consult their own counsel and accountant for advice concerning the various legal, tax and economic matters concerning their investment. The information provided herein does not constitute an offer to sell an interest in the Funds. Such offer can only be made to qualified investors pursuant to the Funds’ Confidential Private Placement Memorandum (“Offering Memorandum”), the Subscription Documents relating thereto and the Limited Liability Company Agreement, as applicable, which set forth the complete terms of the offer.

No representation or warranty (express or implied) is made or can be given with respect to the accuracy or completeness of the information found within this website. Certain information constitutes “forward-looking statements” about potential future results. Those results may not be achieved, due to implementation lag, other timing factors, portfolio management decision-making, economic or market conditions or other unanticipated factors. Nothing contained herein shall be relied upon as a promise or representation whether as to past or future performance or otherwise.