Click here to access this dispatch as a formatted PDF.

Historically, Dispatches from India has been a venue for us to discuss India's broader economic tailwinds and the more nuanced sectoral trends under the surface. We are now adding investment memos for individual securities currently in our portfolio. Recently, our co-portfolio manager Andrei Stetsenko shared Gymkhana's investment thesis for Maharashtra Scooters Limited (NSE: MAHSCOOTER) on the Yet Another Value Podcast with Andrew Walker and we felt this would be the right company to kick off our company specific coverage. Below you will find the podcast followed by our investment memo.

Background

Maharashtra Scooters Limited trades on India’s National Stock Exchange (NSE) under the ticker MAHSCOOTER.

- The company’s Bloomberg ticker is MHSC IN, while its own filings use the acronym MSL; “MAHSCOOTER” is used throughout the rest of this memo.

- Gymkhana Partners has been invested in MAHSCOOTER since April 2024, and was a shareholder in its listed affiliate Bajaj Holdings (BAJAJHLDNG) from 2013 until we sold our last remaining shares earlier this year.

- We re-invested the proceeds from our sales of BAJAJHLDNG into purchases of additional shares in MAHSCOOTER.

- We re-invested the proceeds from our sales of BAJAJHLDNG into purchases of additional shares in MAHSCOOTER.

Our India fund is a shareholder in over a dozen listed Indian holding companies (a.k.a. “holdcos”) trading at very significant discounts to the market values of their stakes in listed underlying operating affiliates.

Listed Indian holdcos

Our India fund is a shareholder in over a dozen listed Indian holding companies (a.k.a. “holdcos”) trading at very significant discounts to the market values of their stakes in listed underlying operating affiliates.

- Among the varied origins of India’s listed holdcos, the most typical began with a successful industrialist seeking to equitably divide his wealth among heirs.

- Other motives included minimizing inheritance taxes by having them levied on opaque and typically significantly undervalued holdcos (rather than on directly-owned shares in underlying businesses).

- Over the generations, some of these conglomerates have devolved into convoluted webs of cross-shareholdings, while others have morphed into professionally-managed, dividend-paying flagships sitting at the apex of their respective groups’ diversified operations.

- Other motives included minimizing inheritance taxes by having them levied on opaque and typically significantly undervalued holdcos (rather than on directly-owned shares in underlying businesses).

- Of course, just because an Indian holdco sells at a discount to its sum-of-the-parts value is not enough to make it a good investment.

- We own the ones we do because they allow us to gain exposure to high-quality, earnings-compounding operating businesses at effective P/Es drastically lower than what we would have paid buying those underlying stocks directly.

When we bring up these undervalued holdcos with our India-based investor friends, we invariably hear that they’ve always traded at wide discounts, that those discounts will likely never close, and that we’re better off simply owning shares in the underlying operating affiliates.

- Well, within our lifetimes, sprawling conglomerates selling at discounts to their sum-of-the-parts values were similarly widespread in the U.S., and attracted similar skepticism from investors.

- Ultimately, though, investor pressure and managerial incentives led to the breakup and favorable revaluation of firms including Gulf and Western, ATI, ITT, United Technologies, GE, and (most recently) Honeywell.

While such a narrowing is not integral to our investment thesis, we wouldn’t be surprised if it happened sooner than some of our aforementioned friends expect.

- In a meaningful but largely under-the-radar development, SEBI (India’s securities regulator) recently unveiled multiple reforms aimed specifically at narrowing the very wide gaps between listed holdcos’ market and book values. These included newly-introduced annual special call auctions intended to improve “price discovery” of otherwise illiquid holdco stocks (further discussed on page 14), as well as streamlined procedures by which a holdco can distribute to its stockholders the holdco’s stakes in other listed companies.

Bajaj Group

Today’s Bajaj Group has its roots in businesses founded in the 1920s by Jamnalal Bajaj, a now quasi-legendary figure who was both a businessman and a prominent independence fighter closely associated with Mahatma Gandhi.

- Born into a poor Rajasthani farming family, Jamnalal was adopted at a young age by Seth Bachharaj Bajaj, a successful trader and distant relative of Jamnalal’s father.

- Jamnalal’s son Kamalnayan Bajaj consolidated the group following the death of his father in 1942.

- In 1945, Bachharaj Trading was founded as a manufacturer of motorcycles, scooters, and auto-rickshaw vehicles.

- In 1960, that entity was rechristened Bajaj Auto Limited and publicly listed.

- In 1965, Kamalnayan’s son Rahul Bajaj became head of Bajaj Group. Rahul oversaw significant growth and diversification at the Group in the decades leading up to his death in 2022.

- In 1975, Maharashtra Scooters Limited (NSE: MAHSCOOTER – discussed in further detail below) was formed as a joint venture between Bajaj Auto and the WMDC, an investment entity owned by the Maharashtra state government.

- MAHSCOOTER became publicly listed that same year.

- In 1987, Bajaj Auto Finance Limited was incorporated, initially with a focus on providing financing for customers of Bajaj Auto.

- In 1994, Bajaj Auto Finance was publicly listed.

- Since 2010, Bajaj Auto Finance has been known as Bajaj Finance Limited (NSE: BAJFINANCE – discussed in further detail on page 6), in a reflection of its evolution into a diversified consumer and small business lender.

In 2007, Bajaj Auto spun out its two-/three-wheeler vehicle manufacturing and financial services businesses into separate publicly-traded companies.

- The spun-out vehicle manufacturing business became a separate publicly-traded company known ever since this reorganization by the name Bajaj Auto Limited (NSE: BAJAJ-AUTO – discussed in further detail on page 8).

- Rahul Bajaj’s older son Rajiv Bajaj, who had taken the reins at Bajaj Auto in 2005, to this day remains the leader of that business, as well as head of the broader Bajaj Group.

- The spun-out financial services business (including the 51.32% majority stake in BAJFINANCE hitherto held by the “old” Bajaj Auto) became a separate publicly-traded company now known as Bajaj Finserv Limited (NSE: BAJAJFINSV – discussed in further detail on page 7).

- All other assets and liabilities of the “old” Bajaj Auto remained with the rump company, which took on its present-day name of Bajaj Holdings & Investment Limited (NSE: BAJAJHLDNG – discussed in further detail on page 9).

- The most important of these remaining assets were the “old” Bajaj Auto’s significant stakes in other Bajaj firms – incl. its 24% stake in MAHSCOOTER.

- The most important of these remaining assets were the “old” Bajaj Auto’s significant stakes in other Bajaj firms – incl. its 24% stake in MAHSCOOTER.

Maharashtra Scooters 1975-2020

In the decades following its founding in 1975, MAHSCOOTER manufactured gearless scooters (i.e., lower-power scooters without the ability to change gears) under the “Chetak” and “Super” brand names.

- In 2006, however, after years of declining sales amid a broader shift in consumer preferences towards multi-gear scooters, MAHSCOOTER discontinued production of geared scooters, while continuing to directly own and operate a smaller manufacturing unit producing pressure die casting dies, jigs, and fixtures for two- and three-wheelers.

In 2002, the “old” Bajaj Auto (i.e., the entity preceding the aforementioned spin-outs that then owned 24% of MAHSCOOTER) began an effort to buy out the 27% stake in MAHSCOOTER held by the Western Maharashtra Development Corporation (WMDC).

- BAJAJ-AUTO offered ₹75/share (vs. a pre-announcement share price around ₹60); WMDC argued that MAHSCOOTER’s holdings of other Bajaj group companies justified a price of at least ₹234/share.

- WMDC had 5 seats on MAHSCOOTER’s 9-person board, giving the state of Maharashtra veto power over major decisions; state politicians ended up pressuring WMDC to “hold out for a better price.”

- BAJAJ-AUTO and WMDC agreed to send the dispute to an arbitrator, who in January 2006 proposed a price of ₹151.56/share.

- While Bajaj was reportedly willing to seal the deal at that price, WMDC appealed the arbitration to higher courts.

- While Bajaj was reportedly willing to seal the deal at that price, WMDC appealed the arbitration to higher courts.

In 2019, BAJAJHLDNG finally bought out WMDC’s 27% stake and became the majority shareholder of MAHSCOOTER.

- In 2019, a ruling by India’s Supreme Court finally ended the 16-year-long legal battle over this matter, allowing BAJAJHLDNG to buy out the 27% stake in MAHSCOOTER formerly held by the state at a price of ₹232/share.

- As a consequence, the Maharashtra state government no longer controls any seats on MAHSCOOTER’s board.

- As a consequence, the Maharashtra state government no longer controls any seats on MAHSCOOTER’s board.

Maharashtra Scooters 2021-present

In 2024, MAHSCOOTER’s board approved the permanent wind-down of all of the company’s remaining wholly-owned manufacturing operations.

- In February 2025, MSL divested the property, plant, and machinery associated with those manufacturing operations for net proceeds (after deducting costs related to workforce rationalizations) of ₹436mm (≈$5mm).

As a result, MAHSCOOTER is now a “pure-play” investment holdco, with the lion’s share of its assets consisting of stakes in businesses that have been and should continue to be direct beneficiaries of the ongoing financialization of Indian households’ savings.

- Dividends have nearly quadrupled from ₹50 per MAHSCOOTER share five years ago to ₹190 per share in CY2025.

- MAHSCOOTER’s dividend payout ratio more than doubled over this period, from ~40% five years ago to an average of ~98% over the past three years.

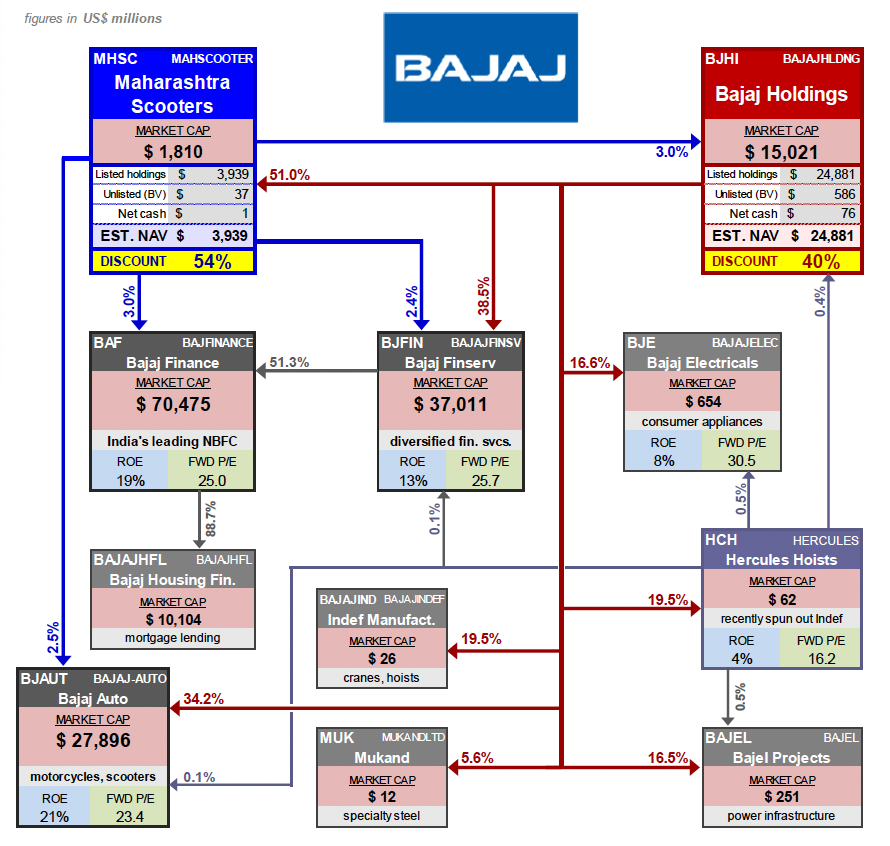

As of this writing, MAHSCOOTER owns:

- 189,746,600 BAJFINANCE shares, equating to a 3.05% stake in Bajaj Finance;

- 37,932,400 BAJAJFINSV shares, equating to a 2.37% stake in Bajaj Finserv;

- 6,879,333 BAJAJ-AUTO shares, equating to a 2.46% stake in Bajaj Auto; and

- 3,387,036 BAJAJHLDNG shares, equating to a 3.04% stake in Bajaj Holdings.

The following pages briefly introduce each of these four underlying businesses.

Underlying businesses

Bajaj Finance NSE: BAJFINANCE

Bajaj Finance Limited (NSE: BAJFINANCE; Bloomberg: BAF IN; also known by the acronym BFL) is India’s largest private-sector non-banking financial company (NBFC), with a >100 million-strong customer base.

- As of November 13, 2025, BAJFINANCE has a market capitalization of ~₹6.3 trillion (≈$70 billion).

- BAJFINANCE has roughly quadrupled earnings per share over the past 5 years; the business generates a ~20% return on equity.

- Widely considered to be one of India’s best-run NBFCs, BAJFINANCE has evolved far from its roots as a financier of Bajaj Auto customers.

- The Bajaj Group maintained strict separation between the managements of BAJFINANCE and BAJAJ-AUTO to ensure the latter was never tempted to drive sales growth by pushing the former to lower lending standards.

- In 2024, BAJFINANCE announced that it would cease origination of loans against BAJAJ-AUTO vehicles altogether.

- BAJFINANCE is now a diversified consumer, business, auto, and home lender.

- In September 2024, BAJFINANCE listed its now ~89%-owned mortgage lending subsidiary Bajaj Housing Finance (NSE: BAJAJHFL).

- In January 2025, BAJFINANCE established a partnership with India’s second-largest mobile telco Bharti Airtel (NSE: BHARTIARTL), giving BAJFINANCE the opportunity to tap Airtel’s 375 million-strong customer base.

- With the Reserve Bank of India having cut benchmark interest rates by 100 basis points year-to-date in 2025, BAJFINANCE can be expected to benefit from widening net interest margins in the quarters ahead.

Bajaj Finserv NSE: BAJAJFINSV

Bajaj Finserv Limited (NSE: BAJAJFINSV; Bloomberg: BJFIN IN; also known by the acronym BFS) is a financial services provider offering insurance, savings products, mutual funds, and more.

- As of November 13, 2025, BAJAJFINSV has a market capitalization of ~₹3.3 trillion (≈$37 billion).

- BAJAJFINSV has roughly doubled earnings per share over the past 5 years; the business generates a ~17% return on equity.

- BAJAJFINSV’s most valuable single asset is its 51.32% majority stake in BAJFINANCE (discussed above).

{kind=link}

- In 2000, BAJAJFINSV formed life insurance and general insurance joint ventures with Munich-based Allianz (ETR: ALV).

- In early 2025, BAJAJFINSV reached an agreement to buy out Allianz’s 26% minority interests in its general and life insurance ventures for approximately €2.6 billion.

- In recent months, Bajaj Allianz Life Insurance and Bajaj Allianz General Insurance were rebranded as Bajaj Life Insurance and Bajaj General Insurance, respectively.

- BAJAJFINSV’s now wholly-owned insurance units are poised to benefit from continued robust growth in India’s insurance market.

- In early 2025, BAJAJFINSV reached an agreement to buy out Allianz’s 26% minority interests in its general and life insurance ventures for approximately €2.6 billion.

- BAJAJFINSV’s other wholly-owned subsidiaries offer exposure to other burgeoning markets including securities brokerage and asset management.

- In a recent interview, BAJAJFINSV head Sanjay Bajaj stated that the company had reached “only about 30% to 40% of its potential market”.

Bajaj Auto NSE: BAJAJ-AUTO

Bajaj Auto Limited (NSE: BAJAJ-AUTO; Bloomberg: BJAUT IN; also known by the acronym BAL) is the world’s fourth-largest manufacturer of two- and three-wheelers.

- As of November 13, 2025, BAJAJ-AUTO has a market capitalization of ~₹2.5 trillion (≈$28 billion).

- BAJAJ-AUTO has roughly doubled earnings per share over the past 5 years; the business generates a ~28% return on equity.

- BAJAJ-AUTO has an ~11% share of India’s overall two-wheeler market.

- The company’s domestic market share has been roughly stable for the past decade, but is down from where it was prior to management’s decision, approximately 15 years ago, to pursue a “differentiation” strategy that has prioritized margins over volumes.

- The company’s domestic market share has been roughly stable for the past decade, but is down from where it was prior to management’s decision, approximately 15 years ago, to pursue a “differentiation” strategy that has prioritized margins over volumes.

- BAJAJ-AUTO’s key competitors in the domestic market include Hero MotoCorp (NSE: HEROMOTOCO), Honda Motorcycle (a wholly-owned subsidiary of Japan’s Honda Motor – TYO: 7267), and TVS Motor (NSE: TVSMOTOR).

- BAJAJ-AUTO is relatively strong in the motorcycle sub-segment but relatively weak in the scooter sub-segment; BAJAJ-AUTO boasts a dominant ~65% share of the small but lucrative niche market for three-wheelers widely used as urban taxis.

- BAJAJ-AUTO is relatively strong in the motorcycle sub-segment but relatively weak in the scooter sub-segment; BAJAJ-AUTO boasts a dominant ~65% share of the small but lucrative niche market for three-wheelers widely used as urban taxis.

{kind=link}

- After a late start, BAJAJ-AUTO is making a concerted push to capture significant share within the burgeoning electric vehicle (EV) segment.

- BAJAJ-AUTO’s EV models now account for ~20% of domestic revenues, and BAJAJ-AUTO rivals TVS Motor (NSE: TVSMOTOR) as India’s leading electric two-wheeler OEM.

- Exports account for ~40% of BAJAJ-AUTO sales volumes.

- The company’s key export markets are Africa, Latin America, the Middle East, and nearby nations in southern Asia.

- The company’s key export markets are Africa, Latin America, the Middle East, and nearby nations in southern Asia.

Bajaj Holdings NSE: BAJAJHLDNG

Bajaj Holdings & Investment Limited (NSE: BAJAJHLDNG; Bloomberg: BJHI IN; also known by the acronym BHIL) is the Bajaj Group’s larger listed holdco.

- As of November 13, 2025, BAJAJHLDNG has a market capitalization of ~₹1.3 trillion (≈$15 billion).

- BAJAJHLDNG sells at an approximately ~40% discount to its SOTP value, the key components of which consist of stakes in the following listed Bajaj firms:

- 38.48% stake in BAJAJFINSV.

- This figure includes BAJAJHLDNG’s 38.35% directly-held stake in BAJAJFINSV, as well as a 0.13% stake held via a 100%-owned unlisted subsidiary of BAJAJHLDNG called Bajaj Auto Holdings Limited.

- 34.21% stake in BAJAJ-AUTO.

- 51.00% stake in MAHSCOOTER.

- See page 12 for an explanation of how we adjust for the two firms’ reciprocal shareholdings.

- Minority stakes in other listed Bajaj cos. incl. Bajaj Electricals (NSE: BAJAJELEC), Bajel Projects (NSE: BAJEL), Indef Manufacturing (NSE: BAJAJINDEF), Hercules Hoists (NSE: HERCULES), and Mukand (NSE: MUKANDLTD).

- 38.48% stake in BAJAJFINSV.

In June 2025, BAJAJHLDNG sold 10.4 million shares of BAJAJFINSV at ₹1,925.20 each, reducing its stake in BAJAJFINSV from ~39.16% to ~38.48%.

- At or around this same time, the Bajaj family’s unlisted Jamnalal Sons holdco offloaded 18.2 million shares of BAJAJFINSV at the same price.

- This recent transaction is indicative of a significant shift in mindset within the Bajaj Group.

- When we met a decade ago with Kevin D’Sa (then CFO of both BAJAJHLDNG and BAJAJ-AUTO), he described BAJAJHLDNG as the “de facto central bank” of the Bajaj Group, and declared that the holdco “will never sell” its shares in the group’s underlying operating businesses.

- When we met a decade ago with Kevin D’Sa (then CFO of both BAJAJHLDNG and BAJAJ-AUTO), he described BAJAJHLDNG as the “de facto central bank” of the Bajaj Group, and declared that the holdco “will never sell” its shares in the group’s underlying operating businesses.

Valuation

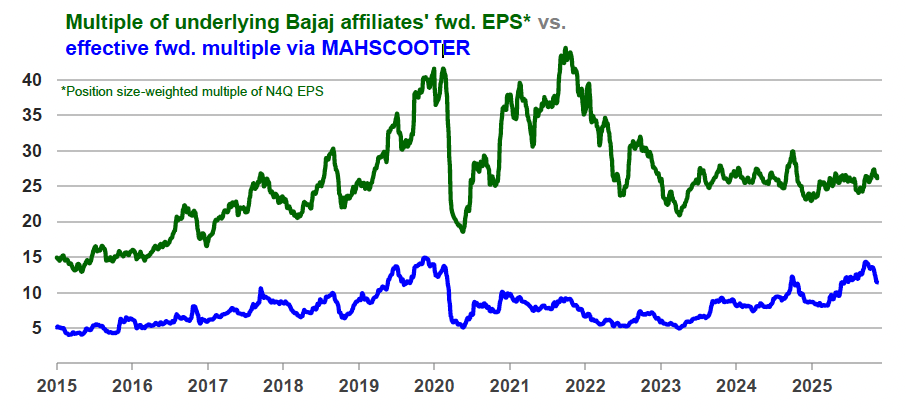

An investor buying MAHSCOOTER at its current ~54% discount to sum of the parts (SOTP) value gains exposure to underlying Bajaj operating businesses at an effective multiple of ~12x those Bajaj affiliates’ FY2027 (fiscal year ending March 2027) earnings – substantially lower than the position-size weighted multiple of ~26x one would pay to buy those stocks directly.

Sum of the parts

As of November 13, 2025, MAHSCOOTER’s equity stakes in other listed Bajaj companies have a combined market value of ~₹350 billion (≈$3.9 billion) – more than double MAHSCOOTER’s ~₹161 billion (≈$1.8 billion) market cap.

Specifically, MAHSCOOTER owns:

- 3.05% of BAJFINANCE, representing ~55% of its overall SOTP value.

- 2.37% of BAJAJFINSV, representing ~22% of its overall SOTP value.

- 2.46% of BAJAJ-AUTO, representing ~17% of its overall SOTP value.

- 3.04% of BAJAJHLDNG, with that stake – after adjusting for reciprocal shareholdings as explained below – accounting for the remaining ~6% of MAHSCOOTER’s overall SOTP value.

MAHSCOOTER’s non-Bajaj Group cash, bank balances, and securities (detailed on page 95 of the company’s FY2025 annual report) add up to a comparatively miniscule ~₹3 billion (≈$38 million).

- MAHSCOOTER’s stated policy is to have a minimum of 90% of assets invested in Bajaj Group companies, with any remainder generally allocated to highly-rated fixed-income securities.

As noted above, BAJAJHLDNG itself holds a 51.00% stake in MAHSCOOTER.

- In our view, the logical way of analyzing reciprocal shareholdings such as these is to treat BAJAJHLDNG’s proportional share of BAJAJHLDNG shares held by MAHSCOOTER as BAJAJHLDNG treasury shares, and vice-versa.

- Adjusted for reciprocal shareholdings using this logic:

- MAHSCOOTER holds an effective 1.49% stake in BAJAJHLDNG, calculated as its 3.04% reported stake multiplied by (1-0.51); and

- BAJAJHLDNG holds an effective 49.45% stake in MAHSCOOTER, calculated as its 51.00% reported stake multiplied by (1-0.0304).

MAHSCOOTER offers a significantly wider to discount to SOTP value than its fellow Bajaj Group holdco BAJAJHLDNG.

- MAHSCOOTER currently sells at an approximately ~54% discount to its SOTP value – or, put another way, MAHSCOOTER’s market cap. equals ~46% of MAHSCOOTER’s SOTP value.

- BAJAJHLDNG currently sells at an approximately ~40% discount to its SOTP value – or, put another way, BAJAJHLDNG’s market cap. equals ~60% of BAJAJHLDNG’s SOTP value.

Multiple of underlying earnings

Another way of viewing MAHSCOOTER’s ~54% discount to sum of the parts value is that it enables an investor to gain exposure to underlying Bajaj operating businesses at a P/E significantly lower than one would pay to own those businesses directly.

Buying MAHSCOOTER at today’s share price allows an investor to own the Bajaj operating businesses discussed above at a position size-weighted multiple of ~12x those underlying businesses’ FY2027 (fiscal year ending March 2027) earnings.

- That is substantially lower than the position-size weighted multiple of ~26x one would pay to buy those stocks directly.

- On a position size-weighted basis, the earnings of the Bajaj businesses in which MAHSCOOTER holds stakes have grown at a compound annual rate of ~23% over the past five years and ~14% over the past ten years – led by BAJFINANCE and BAJAJFINSV, which have been and are set to remain direct beneficiaries of the ongoing financialization of Indian households’ savings.

Potential catalysts

India’s markets regulator SEBI recently unveiled multiple reforms aimed specifically at narrowing the very wide gaps between listed holdcos’ market and book values.

- In June 2024, SEBI introduced a special call auction mechanism for “price discovery” of listed holdcos, and mandated that the such special call auctions be held annually beginning in October 2024.

- MAHSCOOTER was among the holdcos designated as eligible participants in the inaugural special call auction held on October 28, 2024.

- MAHSCOOTER is also among the holdcos set to participate in the second annual special call auction scheduled for October 29, 2025.

- SEBI has also introduced streamlined procedures by which a holdco can distribute to its stockholders the holdco’s shares in other listed companies and/or attempt to buy out minority shareholders.

- The latter involves a simplified offer/counter-offer process deemed successful if the majority shareholder agrees to pay a premium to the market price sufficient to bring its overall ownership above 75%, provided that at least half of publicly-held shares get tendered.

MAHSCOOTER strikes us as the Indian holdco stock where we are perhaps most likely to one day wake up to a headline about mgmt pursuing a delisting or some other process aimed specifically at closing its discount to SOTP value.

- One could easily imagine the Bajaj Group deciding to simply its corporate structure by merging MAHSCOOTER into its majority owner BAJAJHLDNG.

- Of the 49% of shares outstanding not already held by BAJAJHLDNG, more than one-fifth are held by institutional investors.

- Other options available to management include the potential redirection of income from MAHSCOOTER’s investment portfolio (currently being paid out to shareholders via regular dividends) into accretive repurchases of the holdco’s undervalued shares.

As of November 2025, Gymkhana Partners owns shares in one or more of the securities discussed herein, and may trade in and out of these positions without notice.

Legal information and disclosures

The views expressed are the views of the author as of the date indicated on each posting; such views are subject to change without notice. Farley Capital L.P. (Farley Capital)has no duty or obligation to update the information contained herein. Further, Farley Capital makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Any discussion regarding investment returns or financial projections are provided as illustrative examples only and no inference shall be made therefrom regarding the potential for returns on any investment discussed. Moreover, you should be aware that all types of investments involve a significant degree of risk, and wherever there is potential for profit, there is also the possibility of loss.

This content is being made available for informational and educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as financial, legal, or tax advice, or as an offering of advisory services. The information contained herein shall not constitute an offer to sell, or a solicitation to subscribe for, interests in any investment vehicle managed by Farley Capital, which offer or solicitation will only be made to qualified investors and accompanied by a private placement memorandum, subscription agreement, and other related offering documents. Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Farley Capital believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy or completeness of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

This content, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of Farley Capital.

Past performance of Gymkhana Partners and any funds managed by Farley Capital L.P. (collectively, the “Funds”) is not indicative of future results. No representations or warranties of any kind are made or intended, and none should be inferred, with respect to the economic return or the tax consequences from a potential investment in the Funds. Each investor should consult their own counsel and accountant for advice concerning the various legal, tax and economic matters concerning their investment. The information provided herein does not constitute an offer to sell an interest in the Funds. Such offer can only be made to qualified investors pursuant to the Funds’ Confidential Private Placement Memorandum (“Offering Memorandum”), the Subscription Documents relating thereto and the Limited Liability Company Agreement, as applicable, which set forth the complete terms of the offer.

No representation or warranty (express or implied) is made or can be given with respect to the accuracy or completeness of the information found within this website. Certain information constitutes “forward-looking statements” about potential future results. Those results may not be achieved, due to implementation lag, other timing factors, portfolio management decision-making, economic or market conditions or other unanticipated factors. Nothing contained herein shall be relied upon as a promise or representation whether as to past or future performance or otherwise.